Deals

News

Reviews

Advice

Food

Freebies

Generic selectors

Exact matches only

Search in title

Search in content

Post Type Selectors

Search in posts

Search in pages

Deals

News & Alerts

Reviews

Advice

Generic selectors

Exact matches only

Search in title

Search in content

Post Type Selectors

Search in posts

Search in pages

investing

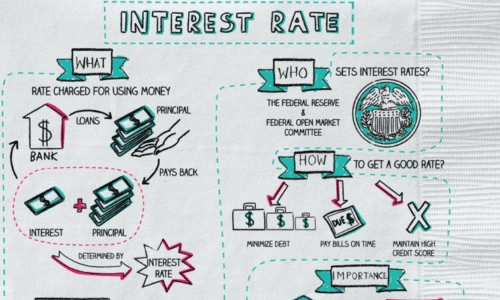

These Cute Napkin Drawings Make Complicated Financial Concepts Easy To Understand

Where should you put your money if you think the market will crash?

5 Handy Lessons Monopoly Teaches Us About Money—Without Us Even Realizing It

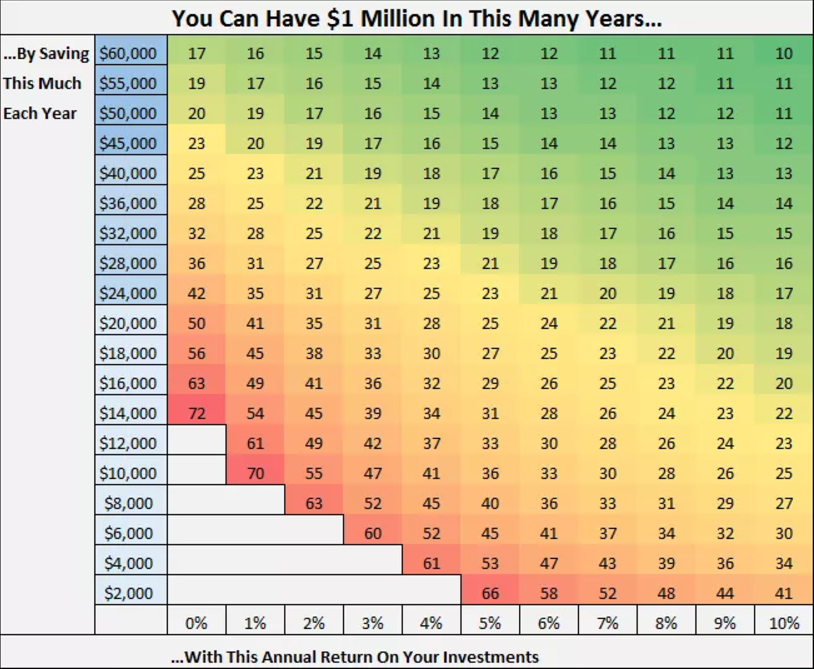

This Chart Shows You How Close You Are To Becoming A Millionaire

Netflix went public 15 years ago this month

11 Expensive Habits That Are A Total Waste Of Money

If You Were The Victim Of This $9M Scam, You Could Get Your Money Back

10 Money Lies It’s Time To Stop Telling Ourselves

This Dad Says He’ll Be Able To Pay For Daughter’s College Education With One Real Estate Investment

From our partners