If you see these 11 items at a thrift store, you should always consider buying them

Want to go thrifting but don't know which items have the most value? Snatch up these 11 finds if you spot them at a secondhand store.

Want to go thrifting but don't know which items have the most value? Snatch up these 11 finds if you spot them at a secondhand store.

Wayfair's Big Outdoor Sale has massive deals on everything from lawn games to patio furniture, but you don't have long to shop.

It's not too late! College-bound students can still apply for scholarships to help pay their tuition for 2024-25. Here are 25 options.

We mined Consumer Price Index data and talked to finance experts to learn what costs less this year, and there's some good news for consumers.

You can head to your local Target to trade in an old, expired or damaged car seat and get a coupon for 20% off a new one during the event.

If you're looking to snag some good deals in April, hit the stores for deals on appliances, summer clothes, running shoes and more.

Average mortgage payments are currently 38% higher than average apartment rents, and the gap is expected to persist.

Learn whether leaving the lights on causes a substantial increase in your energy bill and which lightbulbs are the most efficient.

Dollar Tree announced recently that it would raise the maximum price of its products. Here are the items that will cost you more.

We ordered five items for just $123 from Cupshe, and here's what we thought about this affordable fashion brand.

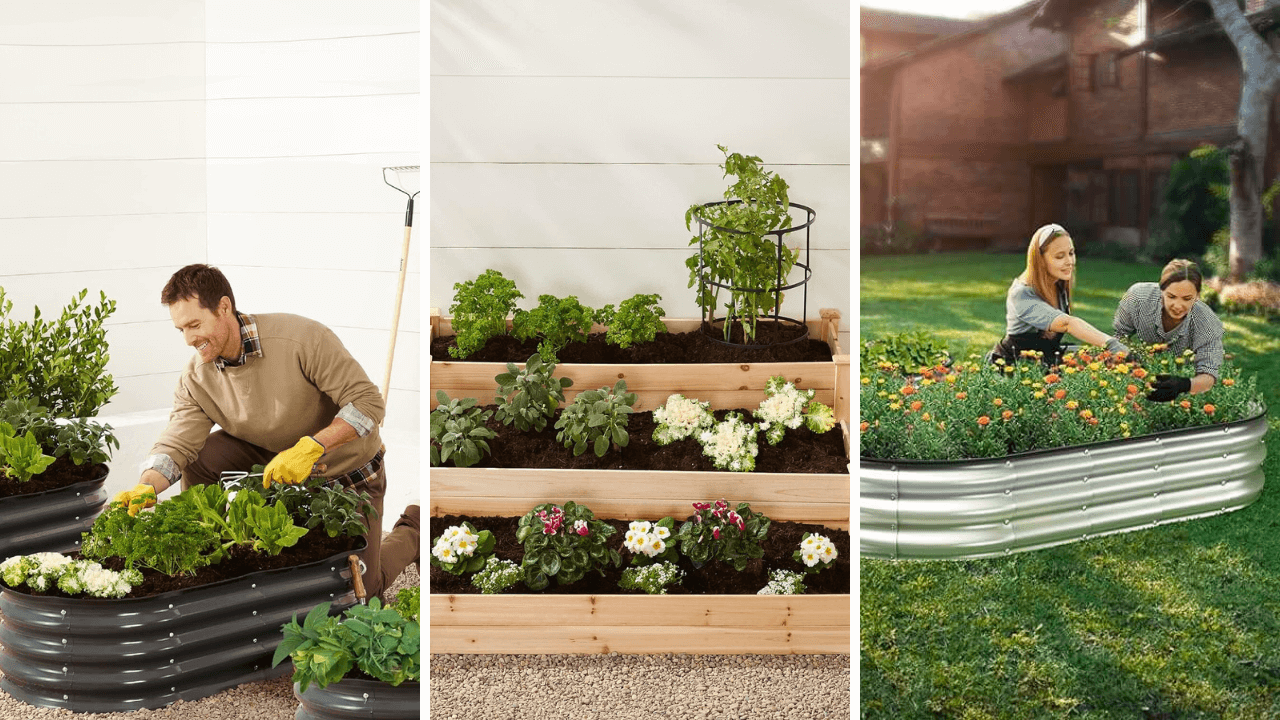

If you're planning to vegetable garden this spring, you can get up to 43% off raised garden beds during Amazon's Big Spring Sale.

A new car seat can be expensive, but these programs might help parents save a bundle with a free car seat for their baby or toddler.

Walmart's spring deals feature over $400 off a patio umbrella, a deal on Apple AirPods, half off luggage and more.

Here are some easy ways to update your home on a budget, whether you're looking to sell or just upgrading for your own comfort.

Spring Break is coming up soon. If you're not traveling, you might be wondering how to entertain your kids all week. Here are some ideas.

Discover the easiest and most difficult places to rent an apartment in America, as well as current market trends that impact renters.

Here are some of the sales and deals you can expect in the month of March, thanks to Easter, Pi Day, St. Patrick's Day, and more.

Submit your claim in a class action lawsuit against Walmart to get a payout based on qualifying store purchases. No proof of purchase needed.

A TikTokker compared monthly living expenses in his city to a month at an all-inclusive resort and found something interesting.

Learn the rankings of the best and worst cities in America for retirement if you don't have money in your savings account.

Taxpayers with outstanding balances may soon be getting a letter notifying them about their debt from the IRS.

If you're an EBT card holder, you can take advantage of free or discounted entry to over a thousand museums nationwide.

If you've got back pain or just a really old mattress, these Presidents' Day mattress sales can get you a new one on a budget.

These password manager services will streamline your efforts to have strong account passwords you can safely share with people you trust.

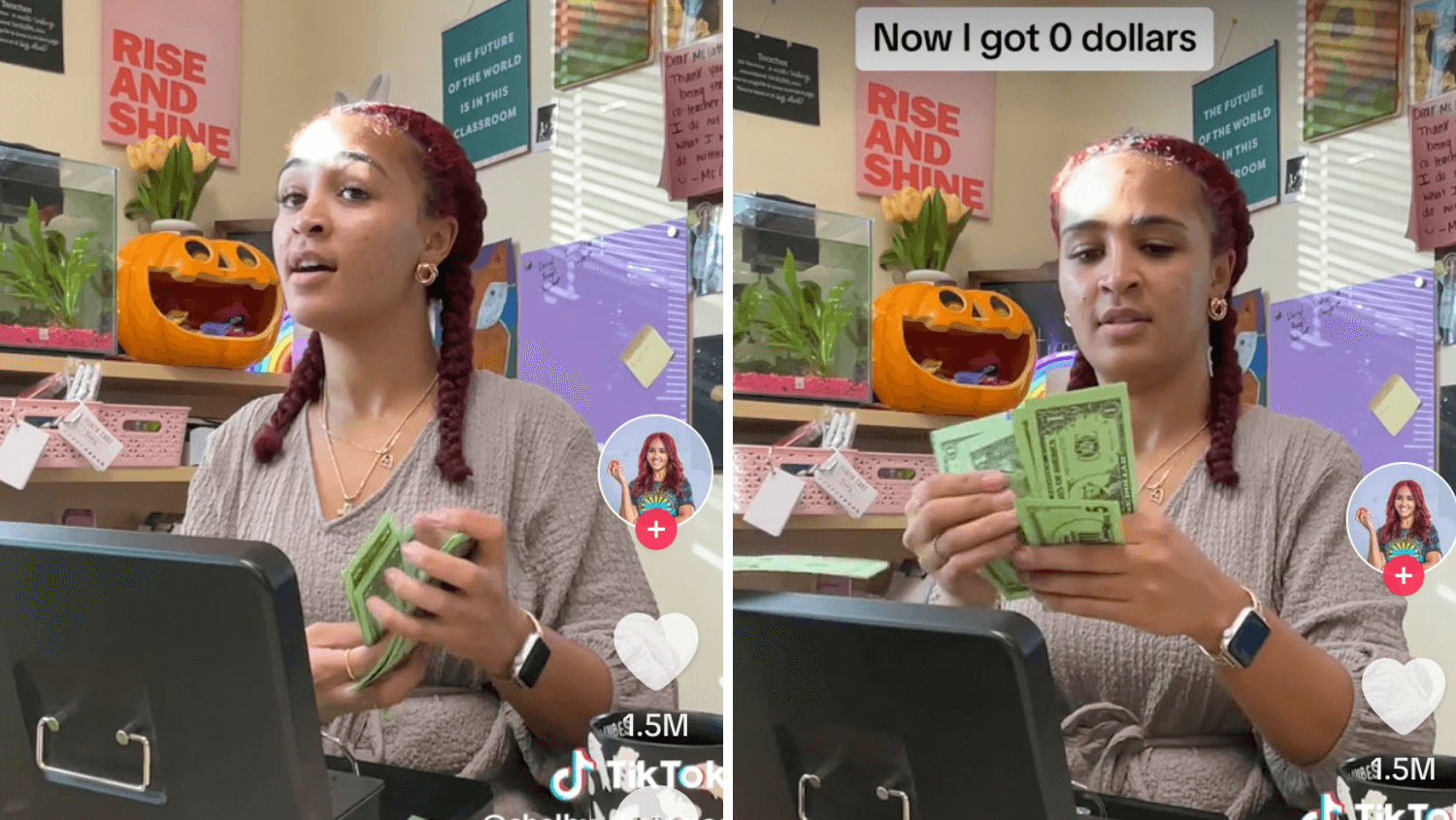

Teacher Shelby Lattimore's viral videos show her teaching her third-grade students about financial literacy by making them pay bills.

Costco Next is a site that only Costco members can access, offering steep discounts on retailers you've seen inside the company's stores.

Whether you're watching for the football or the love story (Taylor's version), there are a number of ways to access the Super Bowl this year.

Teachers can get free dental health kits for 24 students in their classrooms, thanks to this offer from Colgate.

This new financial trend is the opposite of 'quiet luxury': Loud budgeting has people sharing goals to hold themselves accountable.

Household staples are necessary, but they can put a dent in your wallet. Here's how prices compare at Walmart vs. Target vs. Amazon.

February is often centered on Valentine's Day, but there are great deals to be had on everything from mattresses to snow blowers.

A viral TikTok from parents about charging their adult kids rent spurred a discussion about what the right thing to do is in this situation.

Thanks to the Every Kid Outdoors initiative, fourth graders are the VIPs who can get their whole families into national parks for free.

When it comes to finances, many Americans feel stressed about what’s ahead. So they attempt to do too much too quickly.

January is a great time to save on workout gear, kitchen appliances, beauty and skin care products and winter clothing for kids and adults.

Getting into shape can be costly, with many gyms charging upwards of $100 a month. So, we found some of the best ways to exercise on a budget.

Returning a Christmas gift? Return policies have changed, but these tips will help you get the most money back for your return.

Even the dumbest burglars, like the crooks from "Home Alone," know many people will be out of town from now through New Year's Day.

Planning your meals with a slow cooker can help you save on your next trip to the grocery store and even your energy bill. Here's how.

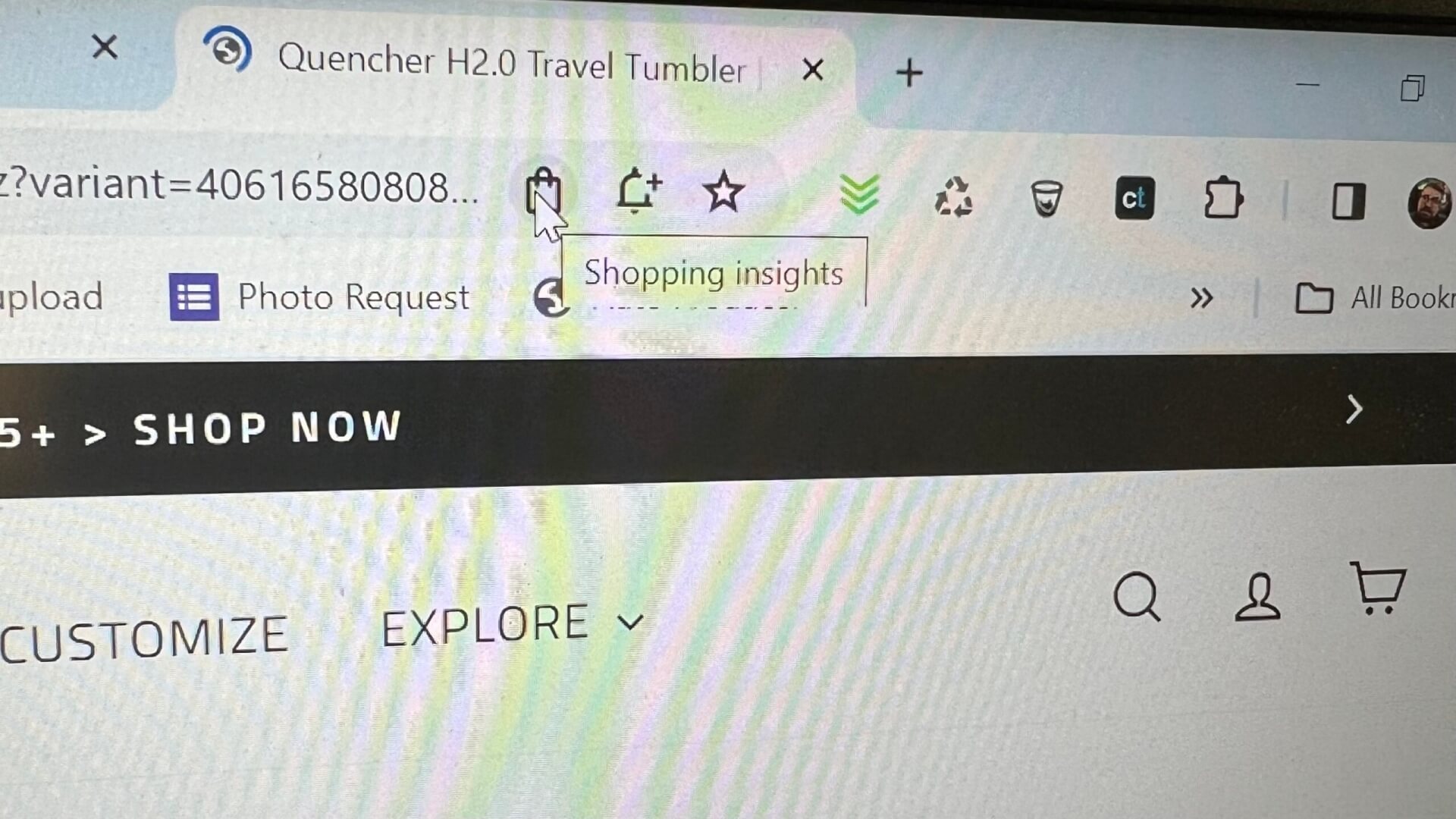

Google launched new shopping features in November that could make finding the best deal for what you want a lot easier.

Even paperback and e-books are expensive nowadays, but apps like Libby offer great ways to read more for free.

Milk glass is a uniquely made type of glass featuring a milky hue, and it's now considered to be an antique collectible.

As you grab those last minute gifts, watch out for counterfeit Apple products, Nike products and more.

Frontier Airlines recently changed its frequent flier program, but savvy travelers can be smart with their airline miles and hotel points.

Our writer compared prices and quality at Dollar Tree, Dollar General and Family Dollar and found a clear winner!

December is a great month to buy thanks to the gifting season, year-end sales, fall inventory clear-outs and one holiday everyone loves.

If you're looking for the best prices as you shop online, check out this app that takes the work out of comparison shopping.

Tax incentives for both new and used EVs are helping to make them less expensive, but there are other money-saving considerations as well.

Just as ceiling fans make practical and energy-efficient solutions in the summertime, they can make a room feel warmer in the cooler months.

These stoppers can be used to block out cold air, loud noises, unwanted smoke and even pesky bugs on French doors, double doors, windows and more.