Deals

News

Reviews

Advice

Food

Freebies

Generic selectors

Exact matches only

Search in title

Search in content

Post Type Selectors

Search in posts

Search in pages

Deals

News & Alerts

Reviews

Advice

Generic selectors

Exact matches only

Search in title

Search in content

Post Type Selectors

Search in posts

Search in pages

retirement

Retirees are returning to the workforce in droves: Here’s why

This city is the No. 1 place to retire in America with no savings

Social Security’s cost-of-living adjustments not enough, report finds

How to become a millionaire by the time you retire

The FIRE movement aims for early retirement through deep frugality

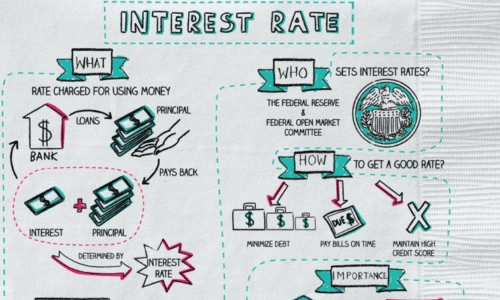

These Cute Napkin Drawings Make Complicated Financial Concepts Easy To Understand

This man plans to spend his retirement at Holiday Inn instead of a nursing home—and here’s how much money he’ll save

Here’s What Life Is Like When You Retire Early

How Social Security Will Change In 2018

The ‘starve and stack’ method could help you save up to $50,000 in two years

Here’s the exact budget of a couple who retired in their 30s

Suze Orman says you should retire at this age

7 Free Ways To Get Personal Finance Planning

These people are actually saving money by living on cruise ships

8 Countries Where You Can Retire On $200K

This 30-Something Couple Is Already Retired—Here’s How They Did It

17 Ways For Retirees To Make A Little Extra Cash

Retirement Savings At Every Age: Here’s How Much To Save

From our partners